MAGA Accounts vs. 529 Plans: Choosing the Right Path for Education Savings

Saving for your child’s future has never been more important…or more complex. With the introduction of MAGA (or “Trump”) Accounts in 2025, many families are asking how these new investment vehicles compare to the familiar 529 college savings plans.

While both accounts aim to help parents and grandparents invest in a child’s future, their design, flexibility, and tax advantages differ in key ways.

🎓 1. Purpose and Intent

529 Plans have long been the go-to option for education-focused savings. Earnings grow tax-free, and withdrawals for qualified education expenses, such as college tuition, books, or housing, aren’t taxed at all.

MAGA Accounts, introduced under the One Big Beautiful Bill Act, were created with a broader goal: to help build wealth for children beyond education. Funds can later be used for a first home, business startup, or retirement.

FedWise Insight: If your goal is specifically education, the 529 plan still offers the most powerful tax benefits. But MAGA Accounts aim for flexibility across life stages.

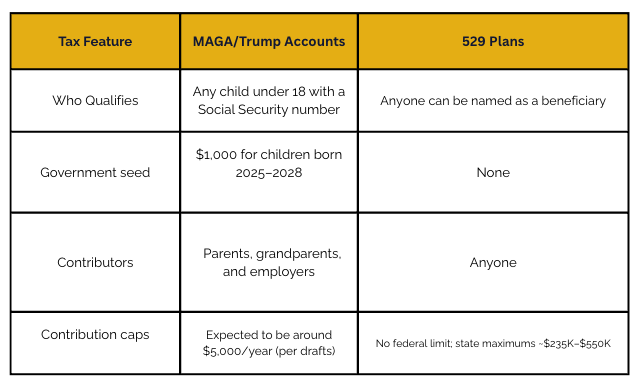

💰 2. Funding and Eligibility

FedWise Tip: MAGA Accounts may complement 529s. The former builds broad wealth, the latter focuses on education tax-free.

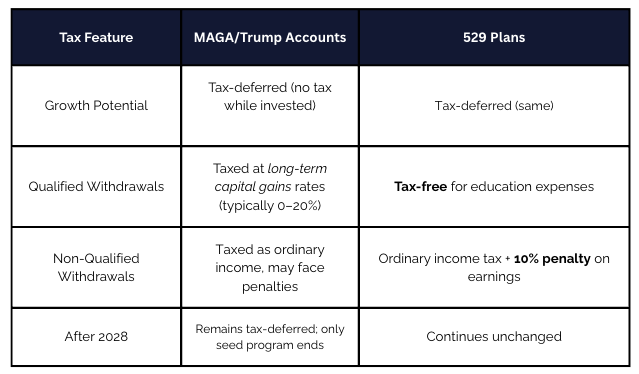

📊 3. Tax Treatment: Growth and Withdrawals

FedWise Insight:529 plans provide unmatched tax-free treatment, but only for education. MAGA Accounts offer flexibility, though future rules could evolve.

📈 4. Investment Choices

MAGA Accounts will likely invest in diversified U.S. stock index funds, similar to retirement or target-date accounts.

529 Plans offer a mix of age-based portfolios and custom fund options, depending on the state program.

Both provide long-term market exposure, but MAGA Account rules will depend on forthcoming Treasury guidance.

🧾 6. Longevity and Policy Outlook

529 Plans are well-established, supported by every state, and backed by decades of precedent. MAGA Accounts are new. Though the $1,000 seed deposit program applies to children born between 2025 and 2028, the account structure itself is intended to continue beyond that period.

Still, because they’re new, implementation details and investment rules are likely to evolve as Treasury releases guidance.

🦉 FedWise Perspective

At FedWise Advisors, we view these two programs as complementary tools rather than competitors:

Each tool serves a purpose, and the best choice depends on your family’s goals, time horizon, and expected education costs.

📞 Ready to Plan Ahead?

If you’d like help deciding between a MAGA Account and a 529, or integrating both into your family’s long-term plan, our team at FedWise Advisors can guide you through the details.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through FedWise Advisors, a separate entity from LPL Financial.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

This material is for informational purposes only and is not intended as tax or legal advice. Always consult your tax professional regarding your specific situation